College may be more expensive than ever before, but the cost of not going to college is pretty steep, as well. For the most part, college graduates earn more, have lower unemployment rates, and are less likely to live in poverty than their less-educated peers. But that doesn’t mean that it’s easy to pay student loans with a recent graduate’s salary (or potential lack thereof, depending on the job market upon graduation). In fact, PayScale’s College ROI Report shows that the highest college loans are likely to be held by the borrowers with the lowest income.

(Photo Credit: weeklydig/Flickr)

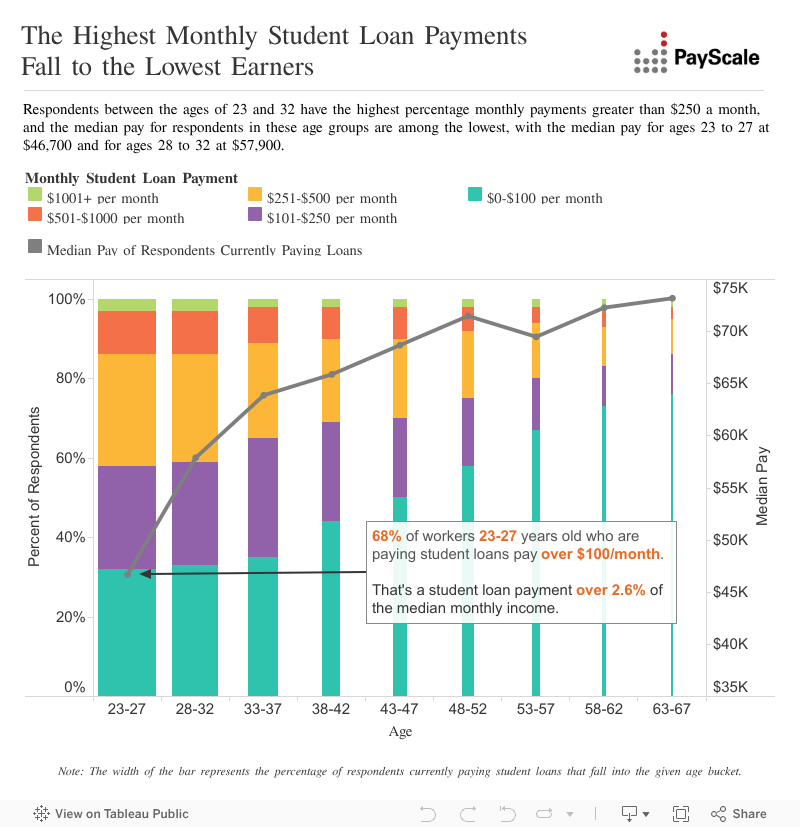

Why are lower-paid borrowers likely to have higher loans? Partly, it’s because recent graduates with less job experience are likely to earn less.

But, age isn’t the whole picture. PayScale’s data also show that household income during college affects loan amounts and earnings after graduation.

Students with lower household incomes during college were more likely to have student loan payments in excess of $250 per month: 39 percent of those in the bottom 25 percent of household income owed that much, while only 27 percent of students in the top 25 percent during school had the same steep loans.

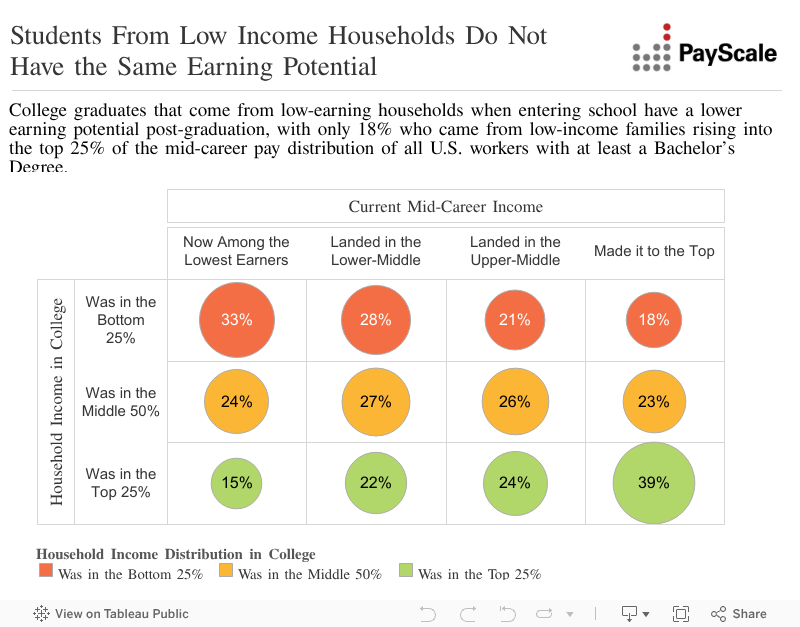

Furthermore, students who were in the bottom 25 percent of income distribution during college were more likely to stay there: 33 percent were in the bottom quarter at mid-career, compared to 15 percent of those students with the highest household incomes during school.

In short, students from lower income backgrounds were more likely to have higher student loans, and less likely to have the income to pay them, and the same goes for recent graduates with less work experience and therefore smaller salaries. It’s not hard to see why newly minted graduates with lower household incomes during school might struggle to climb out of student loan debt.

Tell Us What You Think

Have you had trouble paying your students loans? We want to hear from you! Leave a comment or join the discussion on Twitter.

Leave a Reply